Table of contents:

- Home equity loan vs home equity line of credit: best rates and qualifications

- Home equity loan vs home equity line of credit (HELOC)

- Home equity loan (HEL)

- Home equity line of credit (HELOC)

- Qualifications for home equity loan

- Best rates for home equity loan

Home equity loans, often referred to as HELs, are a popular method for homeowners to leverage the equity they've built in their homes. Whether you're looking to finance a renovation project, consolidate debt, or cover a major expense, a home equity loan can provide the funds you need. But how do you qualify for one, and what are the best rates for a home equity loan? Let's explore.

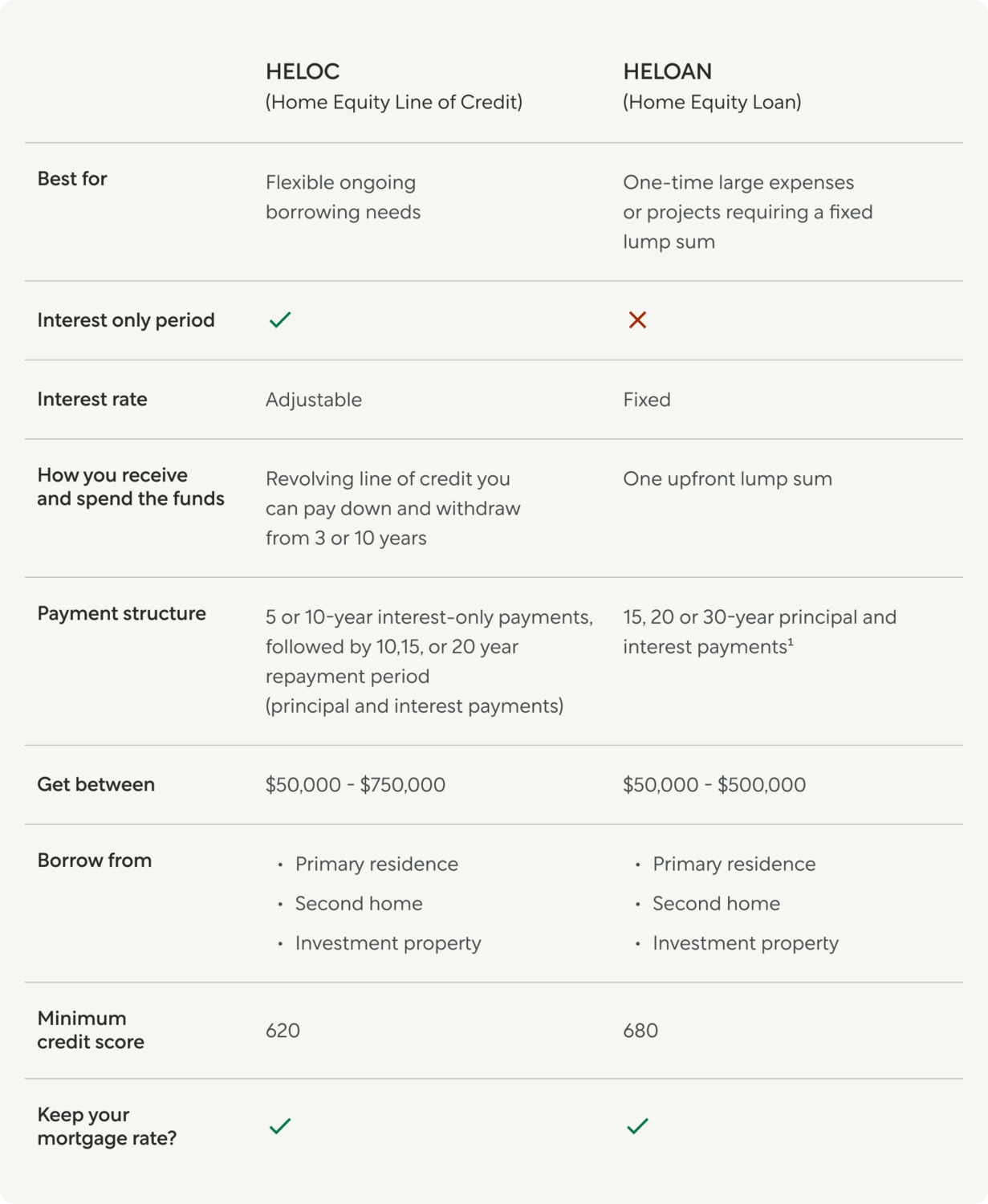

Home equity loan vs home equity line of credit (HELOC)

Before we dive into the specifics of home equity loans, it's important to understand the difference between a Home Equity Loan (HEL) and a Home Equity Line of Credit (HELOC). Both are ways to tap into the equity of your home, but they function differently.

Home equity loan (HEL)

A Home equity loan, or HEL, is a type of loan that allows you to borrow a fixed sum of money against the equity in your home. The loan amount is disbursed in one lump sum, and you repay the loan over a fixed term (typically 15, 20, or 30 years) at a fixed interest rate. This makes HELs a good option for one-time large expenses or projects requiring a fixed lump sum.

Home equity line of credit (HELOC)

On the other hand, a home equity line of credit, or HELOC, is a revolving line of credit that you can draw from as needed during a certain period, known as the draw period. The interest rate on a HELOC is adjustable, and you only pay interest on the amount you've borrowed. This makes HELOCs a more flexible option for ongoing borrowing needs.

Qualifications for home equity loans

Qualifying for a home equity loan requires meeting certain criteria. Here are the typical qualifications:

With Better, you can borrow up to 90% of your home’s equity, giving you more flexibility than traditional lenders that require you to keep 15–20% untouched.

Best rates for home equity loans

The interest rate you'll get on a home equity loan can vary based on several factors, including your credit score, loan amount, and the lender you choose. To get the best rates for a home equity loan, you'll want to:

Remember, the best home equity loan for you depends on your individual circumstances and goals. It's always a good idea to talk to a loan consultant to understand your options and find the best solution for your needs.

More Resources

Home Refinance vs Home Equity Loan: Which Is Right for You?

Everything you need to know about HELOC loans